Award-winning PDF software

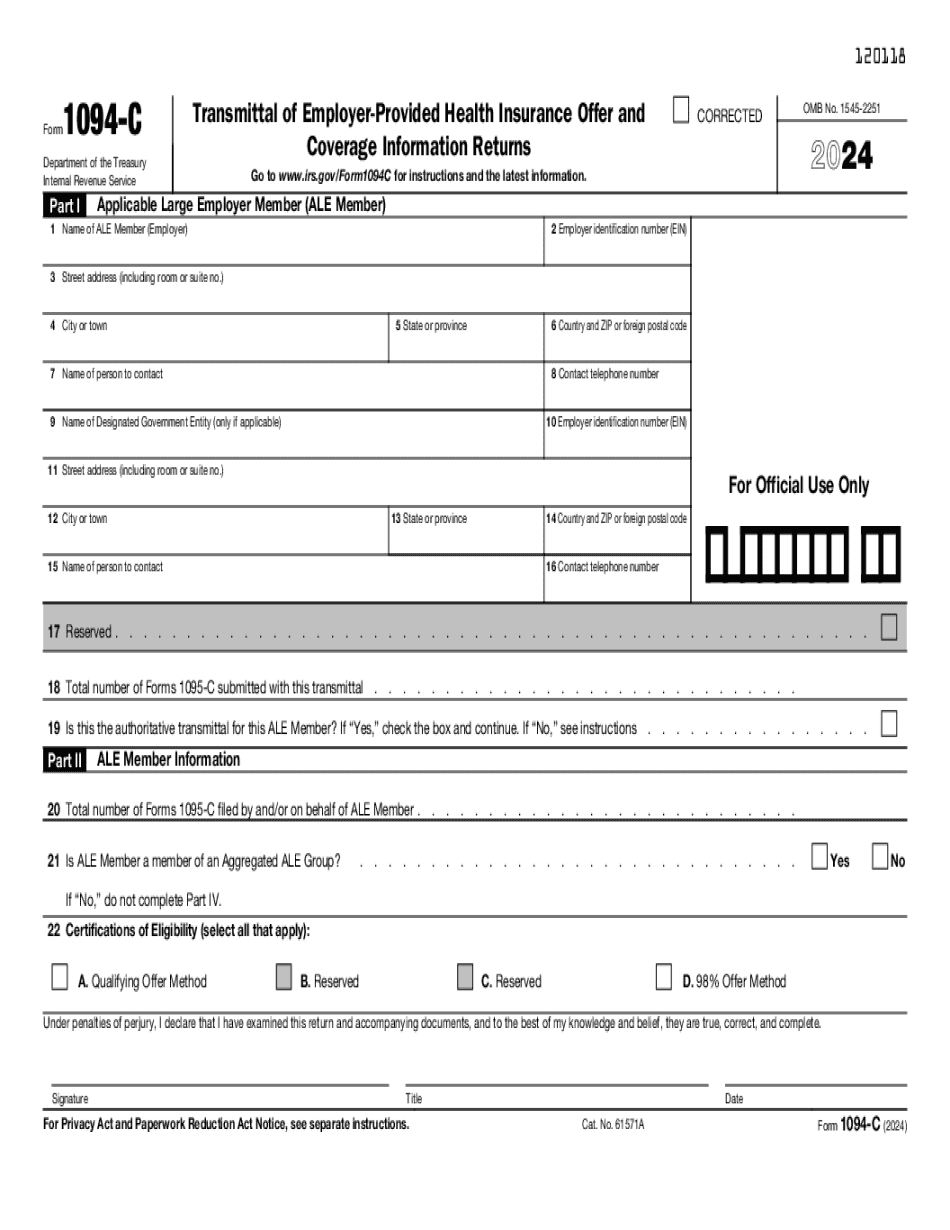

Form 1094-C UT: What You Should Know

Questions and Answers about the Employer Shared Responsibility Provisions The employer shared responsibility provision of the Affordable Care Act (the Act) requires companies with 50 or more full-time workers (including those that are self-employed) to provide coverage for adults without regard to their or their child's age. Employers with 50 or more full-time workers will be responsible for a contribution for each full-time employee whose coverage they do not fully fund. The employer shared responsibility provision does not apply to a family's coverage under a qualified health plan or a health insurance coverage offered in the small business health insurance market. Individuals who are not qualified individuals may still qualify for the coverage provided through their primary care doctor. The employer shared responsibility provision does not apply to short-term disability coverage provided through self-insured plans of an employer's own. The employer shared responsibility provision does not apply to health coverage provided through the exchange or exchange-compliant non-group health plans. However, an employer who has more than 50 full-time employees who enroll through the exchange is required to offer coverage for them. The employer shared responsibility provision does not apply to coverage for an individual's dependent under either of: (1) an individual's current individual federal tax return or (2) a qualifying family arrangement return. The employer shared responsibility provision only applies to a qualified health plan. Employers are not required to offer any other kind of health insurance coverage to their employees other than qualified health plans. In most cases, a person has access to health insurance coverage that is offered through the employer or that is self-funded, but coverage in an employer-sponsored plan or an exchange plan is treated as qualifying coverage for purposes of the employer shared responsibility provision. Employees who fail to maintain coverage provided under their employer's plan may be subject to a month-to-month penalty imposed by the employer for each month during which coverage lapses (exception is for people with qualifying coverage for whom an annual penalty for the non-complying month is only 95 if enrolled on September 11, 2013, through November 11, 2013) or to other penalties imposed by a plan issuer or the law. For additional information, please see our Employer Shared Responsibility Overview page. Additional Information about the Tax Reform Bill's Employer Shared Responsibility Provisions Additional information for the 2025 Tax Reform bill's employer shared responsibility provisions, including the Employee Health Insurance Tax and the Premium Tax Credit for Health Insurance Expansions.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form 1094-C UT, keep away from glitches and furnish it inside a timely method:

How to complete a Form 1094-C UT?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form 1094-C UT aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form 1094-C UT from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.