Award-winning PDF software

form1094-c - internal revenue service

A provider offering to make or provide coverage must also make or provide coverage for all medically necessary items and services for which that provider pays (either directly or indirectly), without regard to whether or not the covered beneficiary was covered, under another health plan or health reimbursement arrangement, during the entire month in which the coverage is effective. Health Reimbursement Arrangements. A provider offering to provide health care items and services through a health reimbursement arrangement must: (1) be certified as a Federal health care provider by the Agency; and (2) meet each of the following conditions: (A) The health reimbursement arrangement will be under a written contract with the health plan or health reimbursement arrangement to be paid by the health plan or health reimbursement arrangement, or jointly with another provider, covering any portion of the provider's cost of providing a given item of health care;.

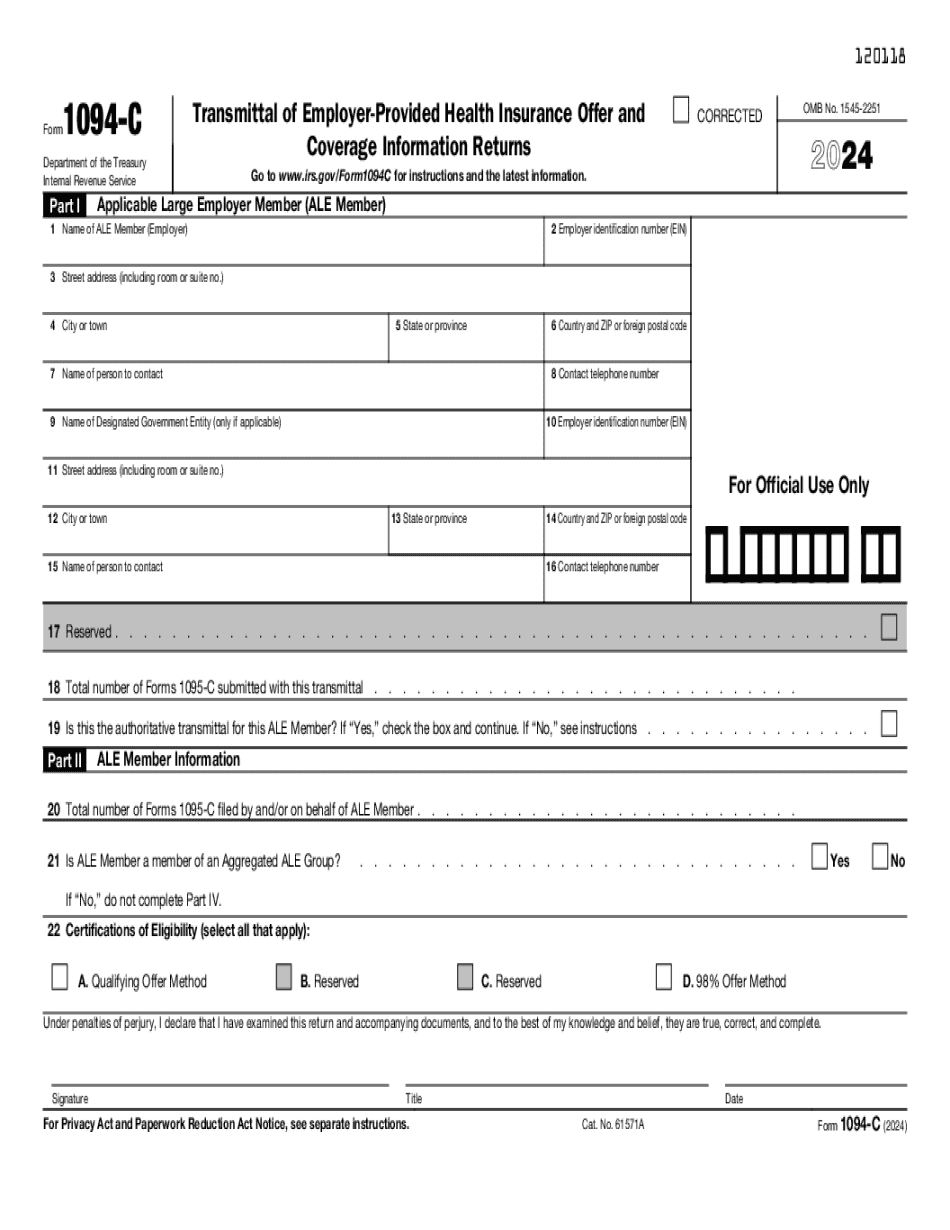

About form 1094-c, transmittal of employer-provided health

Nov 16, 2018 Updated for the 2018 tax filing season.

What is the difference between forms 1094-c and 1095-c?

These forms are used by the IRS to determine income which is taxed under the Internal Revenue Code. The forms are filed and filed quarterly. An analysis of any IRS Form 1094-C is included in this posting. An analysis of the IRS Forms 1094-S and 1095-S (the equivalent to Form 1095-C and 1094-C) is included in this posting. Forms 1094-C and 1095-C are filed as a result of employer-provided health insurance coverage. Those are often the last years of employment where the employee was covered. In certain cases, the employees may have had their coverage for a shorter period of time. The IRS considers that the employee has provided insurance coverage under an employer-sponsored plan for all years of employment and reports these forms on a monthly basis. These forms can be used to calculate the employee's income during a particular month or quarter of tax year and are sent to the.

finally finalizes forms 1094 and 1095 and related

The Forms and Instructions for the Forms 1099-B and 1099-C are on, an electronic data repository of the Internal Revenue Service. 2018 Tax Brackets, Tax Forms and How to Prepare and Use Them The Internal Revenue Service (IRS) is providing a new 2018 tax filing season with a few changes. There are some important changes that you should keep in mind when you fill out Form 1040 and other tax forms. Read the Form 1040 Instructions or the Forms and Instructions for more information. Also, refer to these forms and instructions that have changed: Form 1040-ES (Employment) Form 1040A (Supplemental Disability Income Tax) Form 1040EZ (Exemptions) Form 1040A (Supplemental Disability Income Tax) Form 1040, Form 1040A, the Form 1040EZ, and Form 3949 (Amends) to reflect the latest tax laws and tax rulings. The IRS has also released the new Form W-2G which includes the new 2017 calendar year wage and tax information. Be sure to refer.

What are the deadlines for forms 1094-c and 1095-c in ?

The IRS requires you to complete and file a 1094-C for all net business income (including self-employment income) of at least 10,000 from either an S corporation or a corporation incorporated using a “Pass-through” tax structure (, through which only owners of the business are taxed on the income). The last four columns of Form 1094-C contain additional information: The column designated X includes income from sales, rentals, or contracts for services, and includes all dividends received from S Corporation or partnership income. The column designated C reports business income from any source. This includes income that you received under a contract of sale to a corporation, but also includes income when you received royalty payments for a copyright or patent. This information is available in Appendix E of Part III of Form 1094-C (also available at). Here are some of the common sources of earnings that S corporations will report: Dividends and interest income.